portability of estate tax exemption 2019

The portability feature means that when one spouse dies and his or her estate value does not use up to the total available estate tax exemption the unused portion of the estate tax exemption is then added to the available estate tax exemption for the. 20 million total estate less 2318 million with two estate tax exemptions results in no estate tax liability.

2

The estate tax is a tax on an individuals right to transfer property upon your death.

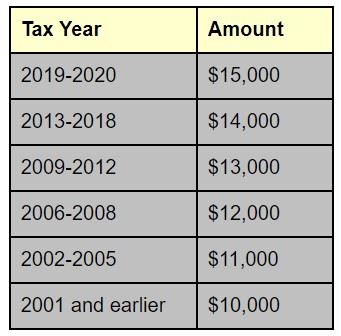

. 2019-2020 15000 2013-2018 14000. Ad Free For Simple Tax Returns Only With TurboTax Free Edition. For those who pass away in 2018 the current amount of 1118 million will still apply.

This privilege in conjunction with the generous federal estate tax exemptions allowed for 2018 through 2025 can allow even large estates to avoid any current federal estate tax liability. On top of this generous amount the IRS also allows for portability of the exemption between spouses. With portability any unused estate tax exemption of the first spouse to die can be carried over to and used by the surviving spouse for federal gift and estate tax purposes.

Portability Federal Estate Tax Exemptions. Why You May Want to Transfer Your Unused Estate Tax Exemption to Your Spouse December 17 2019 by Cathy Lorenz. Electing to use estate tax portability makes a significant difference in your federal estate tax liability.

Thus if a 2019 decedents taxable estate is not more than. When one spouse dies portability allows the surviving spouse to inherit the decedents estate-tax exemption which is currently 114 million for individuals. If it is there is a 40 federal estate tax on the excess.

The federal estate tax exemption will allow you to avoid some taxation as the exemption amount is subtracted from the value of the estate and only the remaining amount will be subject to the federal estate tax. It is recommended that individuals and couples with substantial assets create an estate plan with the help of an attorney to help them minimize their federal tax liability. Donees of gifts from NRAs or foreign estates in excess of 100000 or 16388 in 2019 inflation adjusted from a foreign corporation or partnership must report these gifts to the IRS on Form 3520.

Get Rid Of The Guesswork And Have Confidence Filing With Americas Leader In Taxes. Portability of Estate Tax Exemption. The exemptions are liable to change from year to year so those passing away after 2019 may be subject to different estate tax exemption limits.

For 2019 the exemption has been adjusted for inflation to 114 million per taxpayer and 228 million per married couple. Joan died in 2019 when the married filing jointly estate tax exemption was 228 million. Understanding the portability of the estate tax exemption is crucial to ensuring your spouse has a clear understanding of how portability works.

Estates in excess of the exemption amount are subject to a 40 tax on all assets over the exemption. Get Your Max Refund Today. Phil passes away first when the federal estate tax exemption is 1145 million.

However when one spouse. In 2018 the basic NYS estate tax exemption amount is 5 million and starting 2019 the NYS estate tax exemption amount will be set at 525 million adjusted for inflation. Her joint estate was worth 20 million.

The portability rules provide for the transfer of a deceased spouses unused estate tax exemption deceased spousal unused exclusion amount or DSUEA to a surviving spouse without inflation adjustments. So when Dora passes away the analysis is as follows. The portability of unused estate tax exemption is allowed for persons dying on or after January 1 2011.

Portability can be used to protect the surviving spouse from having to pay steep gift or estate taxes upon a spouses death. In 2022 you will be taxed if the total of the gross assets at hand exceeds 1206 million. Indexed for inflation the TCJA also set out to increase that exemption over time shifting it to 1118 million in 2018 and again to 114 million in 2019.

This works in tandem with the federal gift and estate tax exemption changes the TCJA exacted by way of doubling the existing 5 million exemption to 10 million. The 2019 estate tax exemption will only apply to the estates of individuals passing away in 2019. The law at the time allowed for the portability of the estate tax exemption between a married couple.

The Tax Relief Unemployment Insurance Reauthorization and Job Creations Act of 2010 introduced for the first time the concept of portability of the federal estate tax exclusion between spouses. The federal estate tax exemption is however indexed for inflation and. The surviving spouse would.

In 2019 the federal estate tax exemption was at 114 million. Portability of the estate tax exemption means that if one spouse dies and does not make full use of his or her 5000000 in 2011 or 5120000 in 2012 5250000 in 2013 5340000 in 2014 and 5430000 in 2015 federal estate tax exemption then the surviving spouse can make an election to pick up the unused exemption and add it to the surviving. 6 Thus without New York legislature intervention there is a large taxation discrepancy between New York estate tax rates and Federal estate tax rates.

Each year the government sets a tax exemption limit or exclusion amount for estates under a certain size. If making a portability election a surviving spouse can have an exemption up to 228 million. The portability of the federal estate tax exemption for married couples eliminated the need to plan in such a way.

Thanks to the annual federal gift tax exclusion 15000 for 2018 and 2019 both you and your spouse can make annual gifts to a single recipient up to that amount and reduce the taxable value of your estate without reducing your unified federal estate and gift tax exemption. In the 2010 Tax Act the concept of portability of the unused transfer tax exemption was first introduced in the tax law. The 2019 federal exemption for gift and estate taxes is 11400000 per person.

The Estate Tax Portability Election. The estate of an NRA has only a 60000 not 11400000 estate tax exemption available and no gift tax exemption. Currently the limit is set at 1158 million in combined assets for a decedent who dies in 2020 and is expected to remain at this level until at least 2025.

Under the 2010 Tax Act the unused estate tax exemption could be ported over to the surviving spouse. Because they were married at the time of death no taxes are due since Mark inherits all the assets tax-free. The exemption is 11400000 for 2019 and is indexed for inflation.

Since Joan and Mark are married they are eligible for the portability rules. When enacted it was meant to apply only to estates of.

Estate Planning With Portability In Mind Part Ii The Florida Bar

Tax Portability Transfering Your Tax Benefits From Your Old Homestead To Your New One

The Portability Calculator Ultimate Estate Planner

Will Your Estate Be Taxable In The Future Context Ab

Word Tax With Clock On The Office Workplace Business Concept Getty Images Tax Deductions Capital Gains Tax Irs Taxes

2

Portability Of The Estate Tax Exemption Cdh Law Pllc

Mastering Portability Ultimate Estate Planner

Will Your Estate Be Taxable In The Future Context Ab

Federal Estate Tax Portability The Pollock Firm Llc

Estate Tax Changes Under Recent Tax Acts Tyler Stone Group

Deceased Spousal Unused Exclusion Dsue Portability

Estate Tax Portability Preserving It For The Benefit Of Your Heirs

Portability How It Works For Estate Tax Batson Nolan

750 Tax Pictures Download Free Images On Unsplash

Estate Tax Portability What It Is And How It Works

The Portability Calculator Ultimate Estate Planner

Tackling Tax Issues If You Re An Estate Executor Ferrari Ottoboni Caputo Wunderling Llp

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel